Is this indeed a discrepancy, or am I misunderstanding the article?

You are misunderstanding the situation, since the article is mixing multiple laws that changed over time.

- Currency restrictions (Devisenbewirtschaftung)

- 1931-08-01: RM 3.000

- 1934-09-11: RM 50

- 1934-09-29: RM 10

- Reich Flight Tax (Reichsfluchtsteuer)

- 1931-12-08: for sums over RM 20.000 [§2], 25% [§3(1)]

- 1934-05-18: for sums over RM 5.000, 25% (§3(1) was not changed)

- Fees for money transfer (Dego levy)

- 1934-01: 20%

- 1934-08: 65%

- 1936-10: 81%

- 1938-06: 90%

- 1939-09: 96%

- Ordinance on the registration of property of Jews

- 1938-04-22

- Jewish Capital Levy (Judenvermögensabgabe)

- 1938-11-21: for sums over RM 5.000 [§3(4)], 20% [§4(1)]

The currency restrictions was the amount allowed to be converted to foreign currency and applied to all persons traveling abroad (i.e. also for short visits ; tourist etc.) and are often seen in German passports after 1934.

The Reich Flight Tax applied to all persons leaving the country permanently. A simular law existed between 1918 and 1925.

Fees for money transfer (Dego levy)

Dego-Abgabe (German only)

Wer auf legalem Wege emigrieren wollte, musste seine Wertpapiere und die Verkaufserlöse von Geschäft und Immobilien auf einem Sperrmark-Konto belassen. Der Umtausch vom Auswanderersperrguthaben in Devisen musste von der Deutschen Golddiskontbank genehmigt werden und wurde nur mit einem Disagio vorgenommen, der sogenannten Dego-Abgabe.

Those who wanted to emigrate legally had to leave their securities and the proceeds from the sale of businesses and real estate in a blocked mark account. The exchange of the emigrant's blocked credit into foreign currency had to be approved by the Deutsche Golddiskontbank and was only carried out with a discount, the so-called Dego levy.

Note:

The transfer fee was set by the Deutsche Golddiskontbank and not by law. The Paul Reiss sample quotes 92.5% for November 1938.

Jewish Capital Levy, for German or stateless Jews, based on their worldwide financial assets as of 1938-11-12. For sums over RM 5.000, rounded down to the nearest RM 1.000 [§3(5)]: 20% to be paid in 4 rates of 5% [§4(1,2)]:

- 1938-12-15

- 1939-02-15

- 1939-05-15

- 1939-08-15

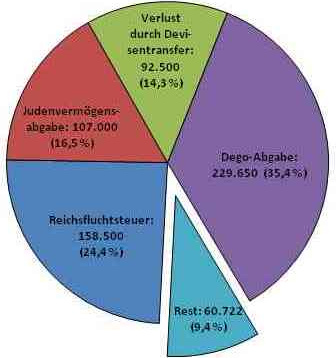

| Sample: Paul Reiss |

Date |

Assets (RM) |

Rate |

Tax/Fee |

Total |

| Reichsfluchtsteuer |

1938-08 |

634.000 |

25% |

158.500 |

158.500 |

| Dego-Abgabe (Transfer) |

1938-11 |

100.000 |

92.5% |

92.500 |

251.000 |

| Judenvermögensabgabe #1/4 |

1938-12-15 |

537.500 |

5% |

26.875 |

277.875 |

| Judenvermögensabgabe #2/4 |

1939-02-15 |

537.500 |

5% |

26.875 |

304.750 |

| Judenvermögensabgabe #3/4 |

1939-05-15 |

537.500 |

5% |

26.875 |

331.625 |

| Judenvermögensabgabe #4/4 |

1939-08-15 |

537.500 |

5% |

26.875 |

358.500 |

| Dego-Abgabe (Transfer) |

1939-09 |

239.219 |

96% |

229.650 |

588.150 |

| Assets |

1940-01 |

60.722 |

|

|

|

Note:

The buying value of the Reichsmark, in 1938, was € 4.30 (as of 2020).

Sources:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}